Specialty medications provide breakthrough, sometimes lifesaving treatments for complex, chronic, and rare diseases. But for self-funded employers bearing the financial burden

of these prescriptions, the high cost of specialty drugs — and the associated stop-loss premium rate hikes — can be challenging to absorb.

Benefit advisors searching for assistance for their self-funded employer clients increasingly turn to alternative funding programs to shift these costs off the pharmacy plan. These solutions may appear attractive to many employers struggling with expensive prescription costs, but they can include unintended consequences — such as a lack of clinical oversight, negative member experiences, and the potential loss of specialty rebate arrangements. At RxBenefits, we’ve seen issues with implementing these financially driven programs. Our preferred partner solutions, paired with our comprehensive Protect suite of clinical products, address these problems.

In this eBook, we’ll examine the questions benefit advisors should ask to identify viable Patient Assistance solutions that reduce specialty costs with minimal disruption.

- Will there be critical clinical oversight?

- How will members be impacted?

- Will adding Patient Assistance impact savings elsewhere?

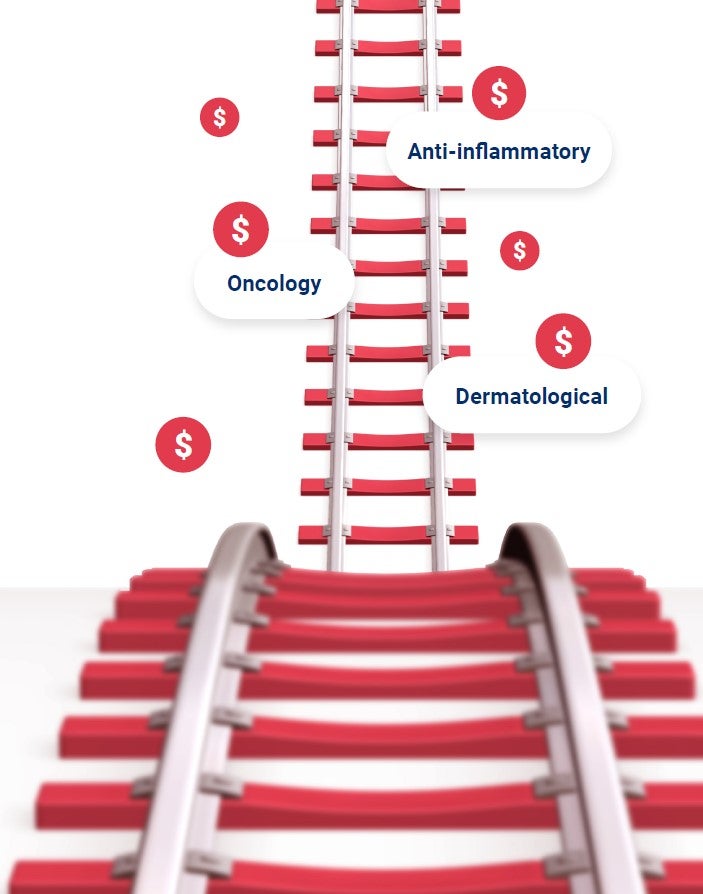

The Likelihood of a High-Cost Claim Increases

Specialty medications may require special handling, close oversight, or supervision from a specialist healthcare provider, which can drive costs higher than traditional medications. These drugs also treat smaller populations, and drug manufacturers often charge more to recoup their research and development dollars when fewer patients will need the treatment.

The top drug classes driving specialty spend are anti-inflammatory, dermatological, and oncology.1 With dermatological and anti-inflammatory drugs, growing usage correlates with direct-to-consumer advertising and label expansion. For oncology medications, prescription growth can be tied to an aging population and an increase in available treatments.

All of this new utilization, plus a growing pipeline of specialty drugs, increases the likelihood of a specialty medication claim impacting a plan.

Inside the Typical Alternative Funding Arrangement

In a typical alternative funding arrangement, employer-sponsored plans try to shift specialty pharmacy spending and catastrophic claim exposure off the plan by excluding coverage for certain high-cost, branded specialty drugs from the prescription drug benefit. A claim for one of those drugs would be denied automatically by the pharmacy benefit manager, and the member would be referred to work with an alternative funding vendor that helps them pursue financial coverage from another source. This could be a manufacturer program, condition-specific charity, foundation, or other philanthropic organization.

Through this process, employers hope the vendor they have selected will help their members access the prescription drug treatment they need. This is highly disruptive to the 2% of members whose specialty medications represent 50% of pharmacy benefit spend. Employers may save money, but alternative funding coverage isn’t guaranteed for the member. Benefit advisors should question whether recommending these types of alternative funding approaches is suitable for their clients or if there’s a better solution.

When Should a Client Add Patient Assistance?

Alternative funding solutions have gained traction because employers want to provide robust pharmacy benefit coverage for their members while protecting their budget from large, unexpected specialty claims. But patient assistance isn’t the right fit for every plan.

Appropriately prescribed medications are essential to a member’s health, and their outcomes can decline when access barriers exist. Employee satisfaction, engagement, and retention can decrease. And the potential loss of rebates can have a meaningful impact on the plan’s net cost, undermining the actual savings.

When educating a client on alternative funding methods, benefit advisors must evaluate the patient mix, drug utilization, the potential of lost rebates, and the need for clinical oversight before making a recommendation. Some employers will benefit financially from Patient Assistance solutions — for instance, if they have many low-income, high-cost claimants taking specialty medications that are eligible for coverage through alternative funding sources.

To determine whether an alternative funding program makes sense for your client — and if so, which one — many factors should be considered.

Determining When an Alternative Funding Program Makes Sense

To recommend alternative funding with a high degree of confidence, benefits advisors should rely on highly skilled pharmacy experts to conduct a detailed review of historical pharmacy claims and perform a comprehensive savings analysis. You should expect this pharmacy resource to employ experts in self-funded benefit plans and stop-loss contracts and to be knowledgeable about many other pharmacy cost-containment programs and vehicles.

To recommend alternative funding with a high degree of confidence, benefits advisors should rely on highly skilled pharmacy experts to conduct a detailed review of historical pharmacy claims and perform a comprehensive savings analysis. You should expect this pharmacy resource to employ experts in self-funded benefit plans and stop-loss contracts and to be knowledgeable about many other pharmacy cost-containment programs and vehicles.

Benefits advisors should consider how alternative funding for specialty medications can affect a PBM contract for a client’s non-specialty drugs and the

possible impact of the resulting lack of clinical oversight. They also need to consider the potential delay in care while funding options are explored, possibly leading to increased medical expenses in the short term.

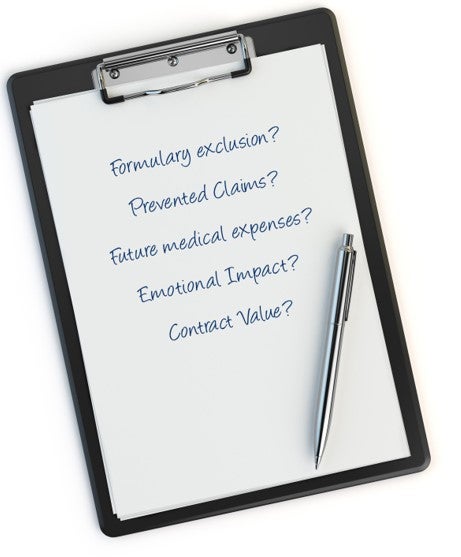

Other considerations include the psychological, emotional, and health impact of excluding specific drugs. Make sure your pharmacy resource can assess these important alternative funding factors:

- Disease states affecting the current population

- Prevalence of high-cost claimants

- Top utilized therapeutic classes

- Efficacy of high-cost medications covered by the plan

- Net cost of medications after rebates

- Plan design concerns

- Effectiveness of lower-cost drug alternatives

- Cost savings through a robust clinical approach to utilization management

- PBM-independent and client-aligned third-party management for prior authorization reviews

- Specialty volume and volatility

Understanding the Unintended Consequences

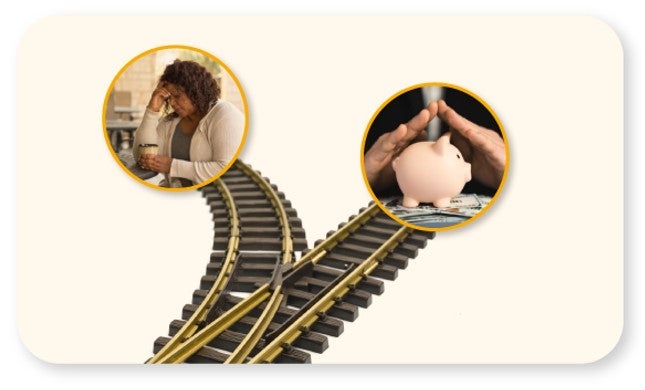

When an employee or plan participant has a serious condition, a choice that seems financially responsible for the employer can have unintended real-world consequences for the member. Using a typical alternative funding option means considering the consequences, such as the psychological and physical repercussions of the delay in treatment.

What happens to the employer-employee relationship when the member endures the potential stress, inconvenience, and embarrassment of applying for financial assistance? At a minimum, the onset of therapy may be delayed while the alternative funding vendor works with the member to secure funding from another source.

In a worst-case scenario, the member might be deemed ineligible, or be deemed eligible but learn that all the available funding sources have been exhausted. What is the emotional, financial, and medical impact of being denied a second time? What should the plan sponsor do in these situations? Often, the employer ends up covering the treatment anyway. Only then is the patient finally able to get started with therapy, with zero savings for the plan and much precious time and goodwill wasted.

Perhaps most troublesome is the thought of sick, lower-earning, uninsured Americans going without treatment. According to a 2021 nationwide poll, as many as 18 million Americans can’t afford their prescribed medications at all, while many others are forced to ration them.2 Many of the dollars some alternative funding vendors tap into were intentionally set aside to assist people with no other options.

Working with Patient Assistance solutions that avoid charity dollars can help alleviate these concerns for plan sponsors. Benefit advisors should look for programs that consider the holistic impact of alternative funding before recommending one of these solutions.

Future Funding and Legislation Changes Could Come Around the Corner

Beyond the moral concern of taking charity dollars to shift plan costs, alternative funding programs that use the funds may be unsustainable. There are no guarantees these funds will stay available for plan sponsors.

Many drug manufacturers and charitable organizations are on high alert regarding employer-sponsored alternative funding programs. They’re beginning to take legal or other action, including removing certain broadly prescribed medications from coverage lists, to ensure their funds are used as intended when these charitable programs were created. The issue could also gain the attention of government entities already interested in regulating pharmacy benefits.

AbbVie — the maker of Humira, a frequently prescribed anti-inflammatory drug — recently changed their program enrollment to disqualify patients working with alternative funding programs from receiving assistance dollars. This is a clear sign that the manufacturer is seeing issues with employer-insured patients tapping into these funds.

As AbbVie and others focus on how these programs are utilized, more changes to qualifications and relevant regulations should be expected.

Address Current & Future Risk With a Strong Partner

From alternative funding to contract negotiations, the support of a strong pharmacy benefits partner can help you guide self-funded employers through the maze of their specialty medication challenges. The right partner should have their eyes fixed on the horizon to anticipate where the next crisis will originate and proactively recommend mitigation strategies and solutions to insulate a benefit advisor’s current and future clients from changing market dynamics.

That partner should have scalable business intelligence capabilities to continuously monitor the evolving characteristics of their clients’ employee populations, ensure the currently implemented cost-containment strategies work in their clients’ best interests, and make data-driven, client-aligned recommendations to optimize economic and clinical outcomes.

They should be able to perform independent, unbiased analyses of all available cost-containment programs in the marketplace to identify and recommend highly viable options. For example, they might bring data-driven condition management programs focused on areas of specialty drug trends such as anti-inflammatory and oncology.

Bridging the Gaps for Your Clients

At RxBenefits, our approach to Patient Assistance solutions works to resolve issues we’ve seen with typical alternative funding programs. The preferred solutions we’ve identified are part of a broader, holistic approach to controlling specialty medication costs. We’ve evaluated the alternative funding benefit administrators in the market and partnered with those that help plan sponsors save money by supporting members in utilizing available drug manufacturer assistance dollars available for high-cost specialty medications.

At RxBenefits, our approach to Patient Assistance solutions works to resolve issues we’ve seen with typical alternative funding programs. The preferred solutions we’ve identified are part of a broader, holistic approach to controlling specialty medication costs. We’ve evaluated the alternative funding benefit administrators in the market and partnered with those that help plan sponsors save money by supporting members in utilizing available drug manufacturer assistance dollars available for high-cost specialty medications.

These solutions provide a clinically sound approach, work within the broader RxBenefits solution offering, have substantial savings potential, and provide a

quality member experience relative to other market alternatives.

Before recommending one of these solutions to a client, our experts conduct a potential savings analysis to ensure their patient and drug mix will benefit. We also consider impacts to other areas of the contract, such as existing rebates on specialty drugs.

These specialty cost control strategies begin with RxBenefits Protect, which includes independently managed prior authorization reviews to ensure the medical necessity and appropriateness of high-cost or frequently misused medications. This ensures we’re rooting out wasteful spending and prescriptions that should never make it through the system before working to obtain alternative funding. It also provides clinical oversight for specialty medications and the other drugs these members are likely taking to coordinate care across the prescription continuum.

Better Paths to Patient Assistance

Keeping with the client-aligned model, RxBenefits doesn’t receive any fees or commissions for implementing these solutions. We offer these solely as a service to our clients.

Keeping with the client-aligned model, RxBenefits doesn’t receive any fees or commissions for implementing these solutions. We offer these solely as a service to our clients.*Note: Program fees apply.

The preferred partners selected by RxBenefits provide retroactive and point-of-sale solutions to best serve the needs of the plan sponsor and the member. For the retroactive solution, the pharmacy fills the prescription at the plan sponsor’s expense after a prior authorization is issued. While the member starts their treatment, our Patient Assistance solution partner reaches out to collect information required for need-based financial assistance. If the member qualifies and funds are available, future prescription refills are dispensed at no cost to the member. If the member doesn’t qualify for funds or funds have

been exhausted, the plan sponsor continues to cover the medication while receiving applicable rebates to offset the drug cost. Retaining the right to collect those rebate dollars can be meaningful when managing plans to the lowest net cost and sets this program apart from others in the market.

When working with the point-of-sale solution, the pharmacy directs the member to the Patient Assistance representatives after the prior authorization is issued. They will be educated about copay assistance and how to enroll in available funding for their specific medication. Once the member completes the manufacturer’s enrollment process, the Patient Assistance solution monitors the pharmacy account on the plan’s behalf. The member receives the medication at no cost to them. The plan is responsible for the remaining balance if the member doesn’t qualify for the funds or the funds have been exhausted. If manufacturer funding is delayed, members can begin treatment using a short fill while funding is pursued. This solution supports member adherence and satisfaction.

Doing What’s Right for Our Clients and Their Members

When plans implement Protect and one of RxBenefits’ preferred Patient Assistance solutions, we deliver:

- Uniquely balanced focus on pharmacy plan savings and member health

- Prospective reporting to audit against preferred partner savings after rebates

- Clinical reviews for appropriateness and safety of applicable medications

- Better coordination with prescribers and members compared to other programs

- Compassionate, award-winning services with a focus on first-call resolution

- Coordination of warm transfers to Patient

- Assistance solution representatives

- Quality control over the member experience

- Retrospective outcomes reporting to audit actual program savings after rebates

Learn more about our Patient

Assistance solutions partnerships

Top Takeaways for Consideration

There’s no single solution for addressing the rising cost of specialty medications. A multifaceted, data-driven, and clinically led approach is warranted to address each client’s specific needs and nuances. While Patient Assistance solutions can help some plans save on specialty drugs, these solutions need to be evaluated for how they fit the company’s benefits philosophy, patient mix, and drug mix. Ultimately, patient assistance may not be the right fit for every plan. Before making a recommendation, consider these factors:

- Fees, lost contract value, and lack of clinical review visibility may negate savings and increase medical utilization and expense. Removing a segment of medications impacts underwriting provisions and changes the terms of the contract. The fees incurred are based on gross savings achieved, which may be based on gross costs, not on what the plan currently pays after rebates. Our thorough, no-cost evaluation will demonstrate the true savings potential for each plan. Our experts will leverage historical claims data, utilization patterns, and more to help you make the right recommendation.

- Many alternative funding solutions need more clinical oversight to ensure access is granted when medically necessary. Putting prior authorization reviews in the hands of independent, unbiased vendors is the only effective way to ensure the clinical necessity and overall appropriateness of high-cost brand and specialty medications. Without this, much of your client’s spending will be wasted on low clinical value medications and inappropriate prescriptions.

- Patient Assistance solutions are only a piece of the specialty medication coverage puzzle. There’s no guarantee that the program dollars will be around forever. Plan sponsors need discounts, rebates, well-negotiated contracts, traditional and supplemental pharmacy stop loss, copay assistance programs, and clinical oversight to keep specialty costs reined in.

Working with a skilled partner can turn pharmacy benefits into a significant point of differentiation that will help you retain and grow your book of business. RxBenefits is the first and only pharmacy benefits optimizer (PBO), serving as a trusted pharmacy adviser to employee benefits consultants and the pharmacy benefits solution provider of choice for self-funded employers. We offer employee benefits consultants a superior alternative to traditional PBM arrangements, combining market-leading purchasing power and contracting expertise with independent clinical advocacy to better manage pharmacy trend and keep the pharmacy benefit affordable. A high-touch service model ensures clients, employees, and dependents receive exceptional care and enjoy a world-class benefits experience.

Sources

1. RxBenefits Book of Business 2022

2. Gallup organization, news release, Sept. 21, 2021